SF’s “Overpaid CEO Tax” Will Hammer Grocery Stores and Coffee Shops

Prop D’s 800% rate hike exempts every major tech company while hitting grocery stores, pharmacies, and coffee shops hard.

TL;DR

Prop D raises taxes ~800% on Safeway, Walgreens, and Starbucks while Google, Meta, and Amazon pay zero.

Under San Francisco’s proposed “Overpaid CEO Tax,” Google pays nothing. Safeway gets hit with an 800% rate increase.

This figure demonstrates a shocking reality: Proposition D, on the June 2026 ballot, would exempt every major tech company in San Francisco and hammer grocery stores, pharmacies, and coffee shops.

Contrary to its proponents’ claims, the “Overpaid CEO tax” is a gift to the companies it pretends to target. All it takes is reading the fine print.

Breaking Down the Tax

Prop D is not a tax on CEO compensation. It is a tax on gross receipts, meaning total business sales in San Francisco. The CEO’s pay determines the rate bracket. The tax itself is levied on the company’s revenue. The CEO doesn’t pay a dime.

The official ballot language asks voters to approve “changing the tax to be calculated using the compensation of all employees, not just those based in San Francisco.” That change matters enormously. Under current law, the pay ratio compares CEO compensation to the median pay of employees in San Francisco. Under Prop D, it shifts to all employees worldwide. For any company with lower-paid workers outside the city, which is nearly every large retailer and chain, this inflates the ratio dramatically.

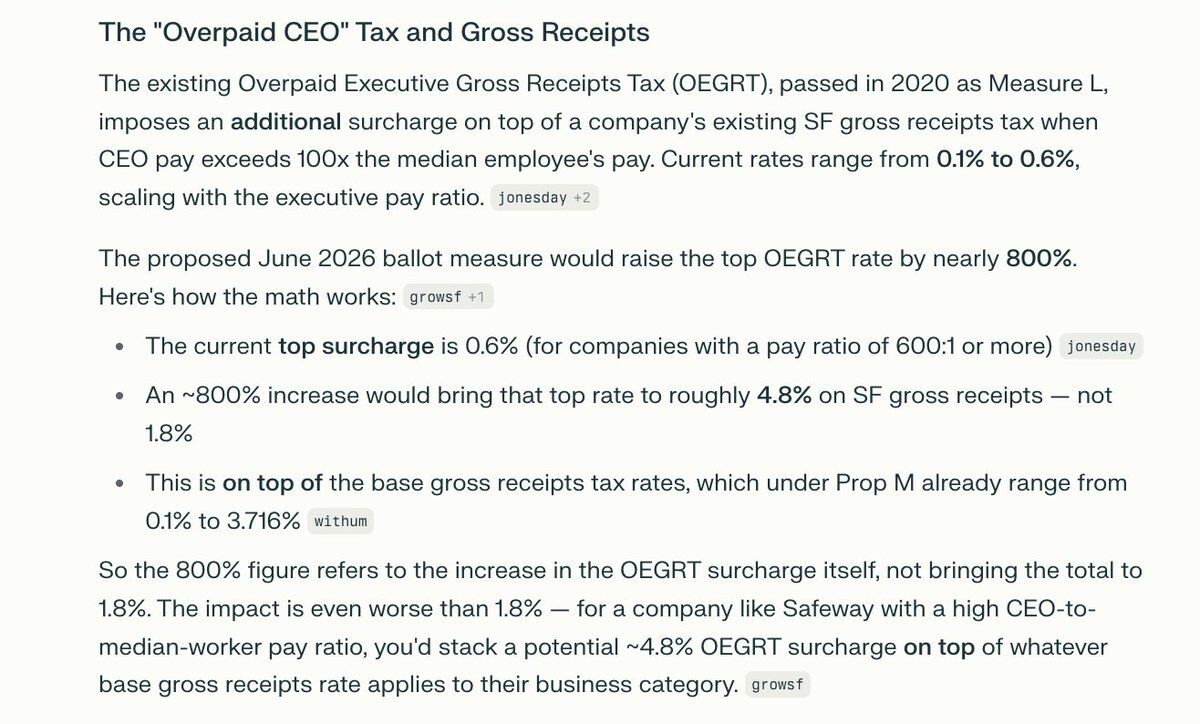

The rate increase is roughly 800% across every bracket. For administrative office taxpayers, payroll-based rates jump from 0.083%–0.499% to 0.75%–4.47%.

Who Actually Gets Taxed

The tax rate depends on the ratio between CEO total compensation and the company’s median employee pay. Companies where the median employee earns a lot, like tech companies paying $300K+, have low ratios and fall below Prop D’s 100:1 threshold — meaning that they are exempt. Companies with lots of hourly workers, cashiers, baristas, pharmacy techs, have high ratios and face the maximum increase.

The actual pay ratios, pulled from SEC proxy statements and the AFL-CIO Executive Paywatch database:

Exempt (ratio under 100:1, zero additional tax):

- Google: 32:1 (median employee pay: $331,894)

- Amazon: 43:1 (median employee pay: $37,181, more on this below)

- Meta: 65:1 (median employee pay: ~$379,000)

- DoorDash: 8:1

Hit hard (ratio over 100:1, ~800% rate increase):

- CVS Health: 299:1 (median pay ~$59,500)

- Walgreens: 410:1 (median pay ~$32,000)

- Safeway/Albertsons: 475:1 (median pay ~$31,781)

- Target: 753:1 (median pay ~$27,100)

- Walmart: 930:1 (median pay ~$29,500)

- Starbucks: 6,666:1 (median pay $14,674)

In other words, a tax marketed as going after overpaid tech CEOs would exempt Google, Meta, Amazon, and DoorDash while hitting Walgreens, Safeway, Starbucks, Target, and Walmart with an ~800% rate increase.

The formula punishes companies for having lots of lower-wage workers, the exact opposite of what proponents claim. A company gets a lower tax bill for paying its median employee $332,000 than for paying its median employee $31,000.

The Amazon Loophole

Amazon is the clearest proof that Prop D’s core mechanism is broken.

In 2023, Amazon’s CEO pay ratio was 6,474:1. Under Prop D, that would have triggered the maximum tax bracket. In 2024, the ratio dropped to 43:1. Completely exempt.

What happened? Amazon’s board eliminated new stock grants for CEO Andy Jassy. His base salary stayed at $365,000. His total reportable compensation fell to $1.6 million. But his actual realized compensation, from previously granted stock awards that vested that year, was $40.1 million.

Amazon’s CEO collected $40 million in real compensation while reporting a 43:1 pay ratio and paying zero additional tax under Prop D.

The Dodd-Frank formula only counts the grant-date value of new awards, not the value of stock that vests from prior grants. Any competent compensation committee can replicate this. Grant large stock awards every other year. In off years, the ratio drops below 100:1. The tax becomes optional for any company with sophisticated lawyers.

Which means it becomes mandatory only for companies that can’t afford the lawyers.

Grocery Margins Can’t Absorb This

According to the Food Marketing Institute, the average net profit margin for grocery stores in 2024 was 1.7%. The industry typically operates between 1% and 3%.

In kitchen-table terms: for every $100 in groceries you buy at Safeway, the store keeps $1.70 in profit. Prop D would take a meaningful chunk of even that.

Safeway’s 475:1 ratio puts them in the 0.748% gross receipts bracket under Prop D. On a 1.7% margin, the tax eats nearly half the profit on every dollar of San Francisco revenue. Meanwhile Whole Foods, part of Amazon with its conveniently gamed 43:1 ratio, pays nothing.

This dynamic is brutal. Safeway raises prices to cover the tax. Customers walk to Whole Foods, which doesn’t carry the burden. Safeway closes the store. The neighborhood loses a grocery store. The city loses the tax revenue entirely. The workers who were supposedly being protected by the “CEO tax” lose their jobs.

Walgreens has already closed 12 San Francisco locations since 2019. An 800% tax increase on the remaining stores is not going to reverse that trend.

The thing that’s perhaps most striking: the labor unions backing Prop D, SEIU Local 1021, Teamsters Joint Council 7, Unite Here Local 2, represent the workers at these exact companies. A tax backed by labor to “fight inequality” will raise grocery prices for people using SNAP benefits to feed their families. The people it claims to protect are the ones who pay.

No Enforcement, No Escape

Two structural flaws make Prop D worse than just bad policy.

First: public companies must disclose pay ratios under Dodd-Frank. Private companies have no such obligation. Prop D applies to private companies too, but the measure specifies no enforcement mechanism, no penalty for misreporting, and no independent verification. A private company claiming 95:1 instead of 105:1 saves the entire tax. It’s an honor system with an clear incentive to cheat.

Second: if Prop D passes, the Board of Supervisors can raise rates further by ordinance but cannot lower them without going back to voters via another ballot measure. If the tax drives businesses out, if it causes store closures, if grocery prices spike, the Board cannot adjust. The only remedy takes months to organize and at least a year to execute.

The Controller’s Office estimates $250–$300 million in annual revenue but warns that actual revenue “could vary significantly” because of the narrow taxpayer base and business relocation risk. The city’s own financial office is suggesting that revenue projections might not survive contact with reality.

Going Against Voters

In November 2024, San Francisco voters approved Proposition M by 69.5%. Prop M reformed the city’s business tax structure, reduced rates for large companies, and raised the small business exemption from $2.25 million to $5 million.

Prop D reverses much of what Prop M did for large companies. Sixteen months after voters approved a more business-friendly tax framework by a nearly 70% margin, Prop D would dramatically increase taxes on the same businesses Prop M was designed to retain.

This is the fifth time since 2018 a ballot measure has altered the gross receipts tax. Stripe left after the first one. Schwab, Square, and McKesson followed.

The message to any business considering San Francisco: the rules change every two years, and always in the wrong direction. It’s like a landlord who keeps jacking rent on tenants who already signed leases, then acts surprised when the building empties out. Businesses need predictability for the same reason tenants do.

Portland tried a similar CEO pay ratio surtax. Portland’s combined tax rate now exceeds New York City’s. Oregon ranks 39th nationally for business environment. Same movie, different city.

The Real Budget Problem

The strongest argument for Prop D is that San Francisco needs money. That part is true.

Mayor Daniel Lurie has warned that “federal and state cuts to health care and safety net funding have set us back and our deficit will reach $1 billion in the coming years.” H.R. 1 alone may cost the city over $300 million annually. The revenue need is real.

But a tax that exempts Google and punishes Safeway is not a revenue solution. It’s a revenue illusion. If the companies most affected simply relocate, as Walgreens has been doing for six years, the city collects nothing and loses everything. The Controller flagged this risk in its own projections.

SPUR recommends voting No on Prop D, noting the 800–900% rate increase would fall primarily on retailers, pharmacies, and grocery stores. The SF Chamber of Commerce, GrowSF, and Mayor Lurie all oppose the measure.

Prop C is the competing measure on the same ballot. It raises the small business exemption from $5 million to $7.5 million, makes smaller adjustments to the executive pay tax within roughly the existing rate range, and does not change the SF-only employee calculation. If both measures pass, the one with more votes prevails. Prop D includes a clause that would void Prop C entirely.

San Francisco genuinely needs revenue. It does not need a tax that exempts Google and punishes Safeway, that any compensation lawyer can dodge, that locks in rates the Board can’t fix, that has no enforcement for private companies, and that reverses what 70% of voters approved 16 months ago. If the businesses most affected by this tax leave, as they’ve been doing since 2019, the city collects zero dollars and loses the grocery stores, pharmacies, and jobs it can’t afford to lose.

Take Action

Share this explainer with every SF voter you know before June 2

Deadline: June 2, 2026

Related Links

-

SPUR Voter Guide: SF Prop D (SPUR)

-

GrowSF: Prop D Raises Taxes (GrowSF)

-

The 'CEO Tax' That Doesn't Tax CEOs (previous coverage) (Garry's List)

-

Proposition M (2024) — Business Tax Reform (SF Treasurer)

-

GrowSF Voter Guide (GrowSF)

Comments (0)

Sign in to join the conversation.